Blog Details

Crude Oil Latest – Multi-Month Trend Remains Positive For Now (Mar 29, 2022)

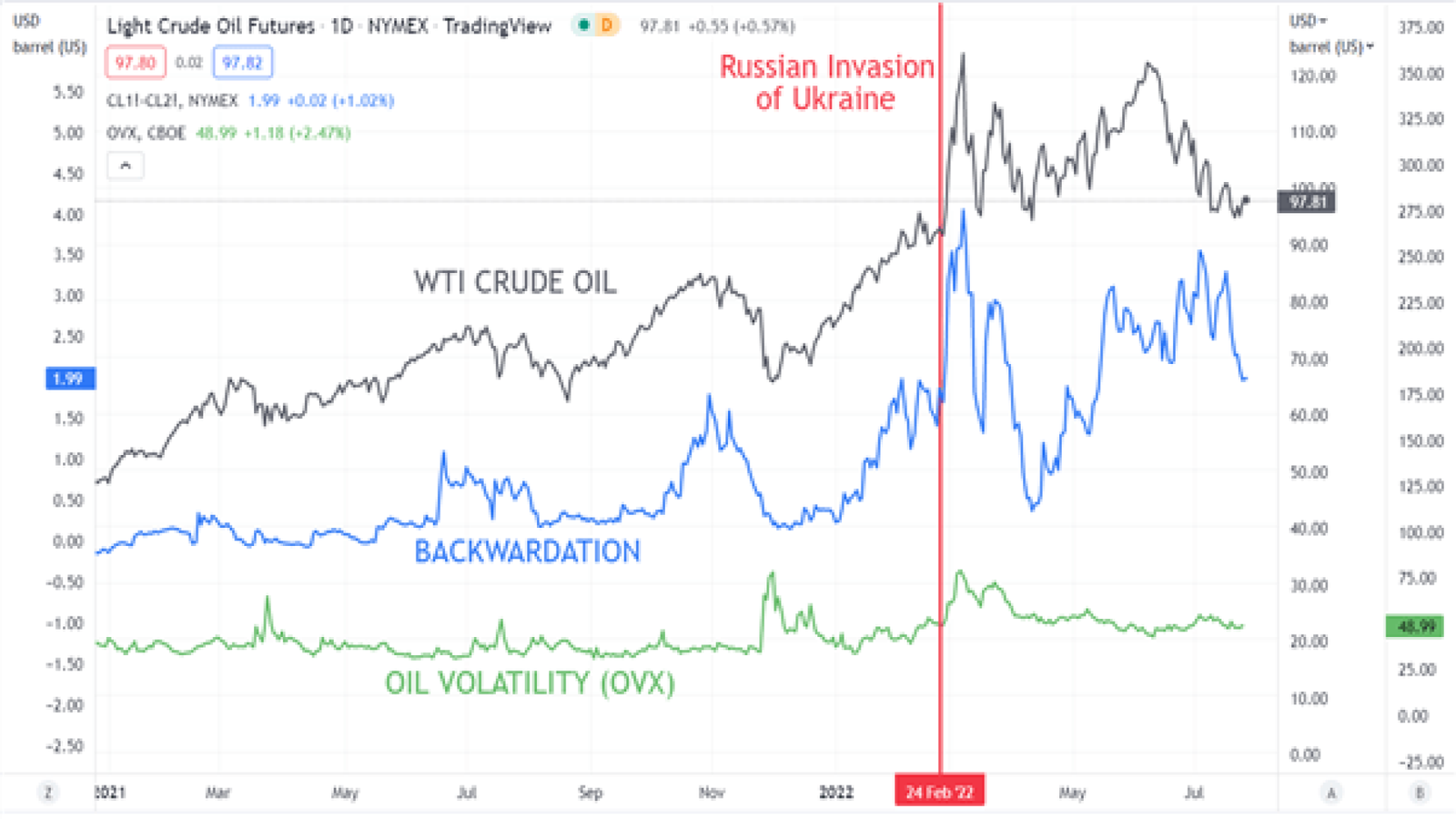

The news at the start of the week that Shanghai will start a phased lockdown due to the rapid spread of the Omicron covid-variant, sent oil tumbling on Monday on fears of reduced demand from China’s main financial hub. Brent crude shed around $9/bbl. as the sell-off took hold with the black gold finishing just off its low print. Today’s price action is slightly more positive with a large part of Monday’s losses pared as buyers once again take control of the market. The lockdown in China will hit demand for oil but with the market already disrupted by the Ukraine crisis and wide-ranging sanctions on Russian oil, the sell-off has opened the door to dip buyers. The latest talks between Ukraine and Russia are if social media is to be believed, marginally more positive with further announcements expected later today. Any deal will take weeks of negotiations, leaving oil demand intact, while if a deal is struck it is very unlikely that Russian oil sanctions would be unwound immediately.

The daily price chart shows oil sticking to its multi-month upward trend. The 50-day simple moving average has provided support all year, and continues to do so, and hovers just above the $100/bbl. level. The ATR indicator shows that oil market volatility remains extreme and is at heightened levels last seen nearly two decades ago. Monday’s low at $106.20/bbl. will provide the first level of short term support before the 50-day sma kicks in at $102.30/bbl. The first level of resistance is seen at $120/bbl.